If you have ever felt overwhelmed by budgeting advice, the 50/30/20 rule simplifies everything into three categories. It is one of the easiest frameworks to follow and it works whether you earn $30,000 or $130,000 a year.

What Is the 50/30/20 Rule?

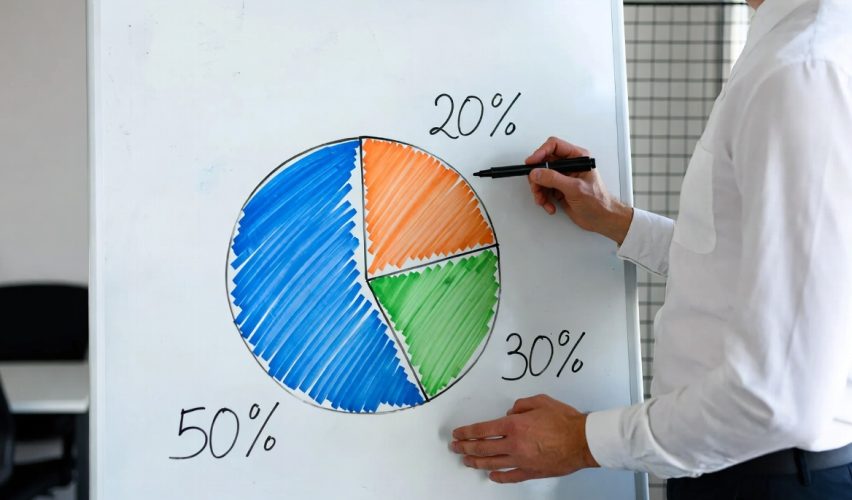

The 50/30/20 rule divides your after-tax income into three buckets. Fifty percent goes to needs — housing, utilities, groceries, insurance, minimum debt payments, and transportation. These are the expenses you cannot avoid.

Thirty percent goes to wants — dining out, entertainment, hobbies, shopping, vacations, and anything else that makes life enjoyable but is not strictly necessary. This is where lifestyle choices live.

Twenty percent goes to savings and extra debt payments — emergency fund contributions, retirement savings, investments, and paying down debt faster than the minimum. This is the money that builds your future.

How to Calculate Your Numbers

Start with your monthly take-home pay. If you earn $4,000 after taxes, your breakdown looks like this: $2,000 for needs, $1,200 for wants, and $800 for savings and debt repayment.

If you are paid biweekly, multiply your paycheck by 26 and divide by 12 to get your true monthly income. Many people make the mistake of multiplying by 2, which actually underestimates their annual income by about $3,000.

Write down your current spending and see where it falls. Most people discover their needs category is closer to 60 or 70 percent, which means the other categories get squeezed. This is normal — and it is exactly where the framework helps you identify what needs to change.

Breaking Down the 50 Percent: Needs

Needs are expenses that you must pay regardless of your lifestyle choices. If you stopped going out, canceled all subscriptions, and lived as simply as possible, these are the bills that would remain.

- Rent or mortgage (including property tax and insurance)

- Utilities: electricity, water, gas, trash

- Groceries (not dining out — that is a want)

- Health insurance and out-of-pocket medical costs

- Car payment, gas, and auto insurance

- Minimum debt payments on all accounts

- Childcare if required for work

If your needs exceed 50 percent, you have two options: increase your income or reduce your largest fixed costs. Housing is usually the biggest lever. If rent consumes 40 percent of your income alone, the entire framework breaks down. Consider whether a move, a roommate, or refinancing could bring that number closer to 25 to 30 percent.

Breaking Down the 30 Percent: Wants

This is the category people feel most guilty about, but it is essential. A budget without room for enjoyment is a budget you will abandon. Wants include restaurants, coffee shops, streaming services, gym memberships, hobbies, travel, new clothes beyond what is strictly necessary, and gifts.

The key distinction between needs and wants is this: would you survive without it? You need food, but you do not need takeout. You need transportation, but you do not need a brand-new car. You need clothes, but you do not need designer brands.

If you are trying to pay off debt or build savings faster, the wants category is where you can temporarily cut back. But do not eliminate it entirely. Keep at least 10 to 15 percent for wants even in aggressive saving mode, or burnout will set in.

Important distinction: Minimum debt payments are a need. Extra payments above the minimum are savings/debt reduction and belong in the 20 percent category. This prevents you from counting aggressive debt payoff as a need and squeezing out all enjoyment.

Breaking Down the 20 Percent: Savings and Debt

This category is where financial progress happens. It includes contributions to your emergency fund, 401(k) or IRA deposits, brokerage account investments, extra payments on student loans or credit cards, and saving for specific goals like a down payment.

If you have high-interest debt (credit cards, payday loans), prioritize paying that off before building investments. The math is simple: if your credit card charges 22 percent interest, paying it off is like earning a guaranteed 22 percent return. No investment consistently beats that.

Once high-interest debt is gone, split this 20 percent between your emergency fund (until you reach three to six months of expenses) and retirement savings. If your employer matches 401(k) contributions, always contribute enough to get the full match — it is free money.

When the 50/30/20 Rule Does Not Work

This framework is a starting point, not a rigid law. It does not work perfectly for everyone, and that is okay. Here are common situations where you may need to adjust the ratios.

High cost-of-living areas. If you live in San Francisco, New York, or another expensive city, your needs may consume 60 percent or more. Adjust to 60/20/20 and focus on growing your income over time.

Very low income. When you are earning minimum wage, survival takes priority. Your split might be 70/15/15 or even 80/10/10. That is fine. Any amount in savings is progress.

High earners. If you earn well above average, you probably do not need 30 percent for wants. Consider shifting to 50/20/30, putting the extra 10 percent into investments that compound over decades.

Aggressive debt payoff. If you are committed to becoming debt-free quickly, try 50/20/30, flipping wants and savings. Live more simply for 12 to 24 months and throw everything at your debt.

How to Get Started Today

Pull up your bank statement from last month. Categorize every transaction as a need, want, or savings/debt payment. Calculate the percentages. You now know exactly where you stand relative to the 50/30/20 framework.

Do not try to fix everything at once. Pick the category that is furthest off track and make one adjustment this month. Maybe you cancel two subscriptions you forgot about. Maybe you cook at home one extra night per week. Small moves, repeated consistently, add up to major changes over a year.

The 50/30/20 rule is not about perfection. It is about having a simple, memorable framework that guides your decisions without requiring a spreadsheet and two hours every weekend. If you can remember three numbers, you can manage your money.

Start with last month’s bank statement

Categorize your spending into needs, wants, and savings — then adjust one category this month.

Finance Helper Hub may receive compensation when you click links on this page. All information is for educational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified professional before making financial decisions.

Get Free Financial Tips Delivered to Your Inbox

Join thousands of readers learning to take control of their money. No spam, unsubscribe anytime.

We respect your privacy. Read our Privacy Policy.